VP Sara Duterte faces P6.77-billion financial scrutiny

Transaction records totaling P6.77 billion linked to Philippine Vice President Sara Duterte and her husband are at the center of an impeachment trial. While not direct proof of corruption or ill-gotten wealth, the figures raise questions about their declared assets.

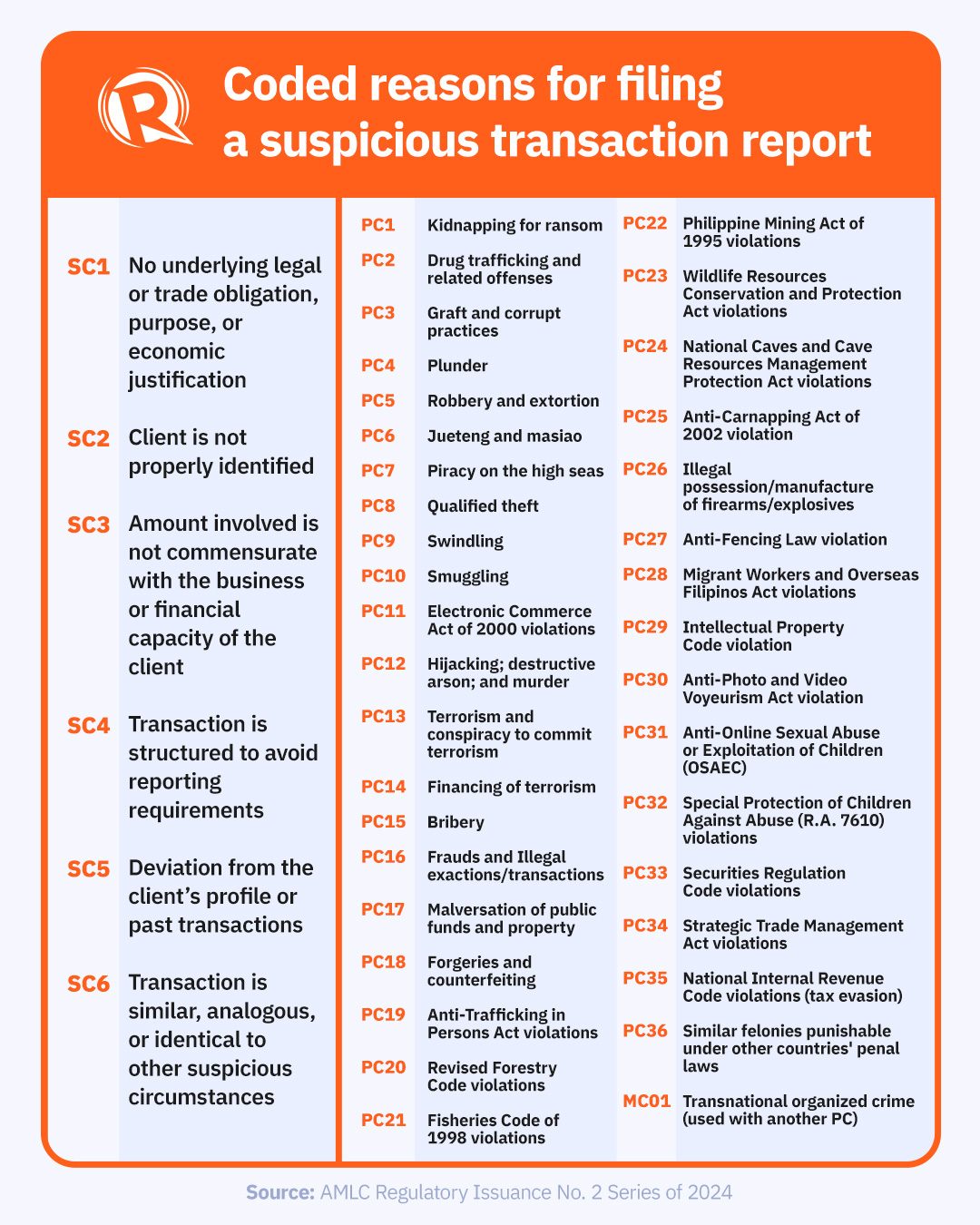

The AMLC reports do not prove corruption. The SALNs do not prove concealment. The BIR records do not yet prove tax violations. But together they pose a financial question that no impeachment court can simply overlook. The temptation is to treat the P6.77-billion figure linked to Vice President Sara Duterte and her husband, lawyer Manases Carpio, as the smoking gun of the impeachment trial. That would be a mistake. The figure does not mean the couple accumulated P6.77 billion, nor does it establish money laundering or unexplained wealth. It represents the cumulative value of transactions reported by financial institutions over nearly two decades, and the same money can be counted repeatedly as it moves through multiple accounts. Transaction volume is not the same as personal wealth. Yet, dismissing the figure on that basis would be equally erroneous. What the impeachment court should look into is whether those billions in financial activity can be reconciled with Duterte’s declared wealth, her tax records, and the financial disclosures required of every public official. According to testimony before the House justice committee, the Anti-Money Laundering Council (AMLC) received 630 covered transaction reports and 33 suspicious transaction reports involving Duterte and Carpio from 2006 to 2025. Out of the reported total, 313 covered transaction and 17 suspicious reports involving Duterte accounted for approximately P3.77 billion, while 317 covered transaction and 16 suspicious reports involving Carpio represented another P2.99 billion. Those figures deserve careful interpretation. Under the Anti-Money Laundering Act, a covered transaction is generally a cash transaction exceeding P500,000 in one banking day that is automatically reported by financial institutions. A suspicious transaction is different. It is reported because a bank believes it may lack a legitimate economic purpose, appears inconsistent with a customer’s financial profile, or exhibits characteristics associated with possible unlawful activity. A suspicious transaction report, however, is not a judicial finding of guilt. It is an alert requiring further examination, not a conviction. We have to understand this because the prosecution cannot simply point to P6.77 billion and ask the Senate to infer corruption. Money laundering under Philippine law requires more than unusual banking activity. Authorities must connect the transactions to the proceeds of an identified unlawful activity. The Supreme Court has consistently required proof of a direct connection before freezing or forfeiting assets. While the AMLC reports establish that significant financial activity has taken place, they cannot verify, by themselves, where the money came from or whether it was illegally obtained. The financial picture becomes considerably more compelling when the AMLC data is compared with Duterte’s Statements of Assets, Liabilities and Net Worth (SALN). Publicly available SALNs reportedly show her declared net worth increasing from about P55.6 million in 2019 to P88.5 million in 2024, while declaring no cash on hand and no bank deposits during those years. A SALN, admittedly, is a year-end snapshot of assets and liabilities, whereas AMLC reports measure transactions occurring throughout the year. Someone may legitimately receive substantial funds, invest them, purchase property, or repay obligations before the end of the year. That accounting distinction is real. However, if accounts associated with Duterte generated billions in reportable transactions while successive SALNs reflected no cash or bank deposits, the apparent inconsistency is substantial enough to require explanation rather than political rhetoric. This is where the Bureau of Internal Revenue (BIR) records could become the most important evidence in the impeachment trial. Unlike AMLC reports, which merely track financial movement, tax returns reveal whether income was declared and taxes were paid. Must Read What Sara Duterte’s traveling BIR box says about Philippine tax secrecy They can distinguish business receipts from personal income, loans from earnings, capital gains from ordinary deposits, and corporate transactions from individually owned assets. The BIR delivered Duterte’s tax records to the House justice committee under seal, but lawmakers voted against opening them, leaving the issue for the Senate impeachment court. Consequently, no one can honestly claim today that the records prove tax evasion or unexplained wealth because the public has not seen them. That uncertainty should not weaken the prosecution’s case; it should sharpen its focus. The Senate’s task is not to determine whether P6.77 billion sounds excessive. It is to determine whether every material inflow can be matched with a lawful source and whether those sources are consistent with Duterte’s SALNs, tax filings, and legitimate income. If the transactions arose from property sales, there should be supporting deeds and tax payments. If they represented loans, there should be promissory notes and repayment schedules. If they belonged to corporations, audited financial statements should establish that the funds were corporate rather than personal. If they reflected legitimate professional or business income, they should appear in tax returns. The defense, meanwhile, is entitled to insist that confidentiality laws governing AMLC reports and taxpayer information be respected. Those protections exist for good reason. But confidentiality cannot become immunity from constitutional accountability. The Senate, sitting as an impeachment court, possesses the authority to compel relevant evidence even while protecting legitimate privacy through appropriate procedures. Legal protections of financial secrecy should shield innocent account holders from unwarranted public exposure, but they should not prevent constitutional institutions from determining whether high-ranking government officials have breached their public trust. Ultimately, the impeachment case is unlikely to rise or fall on a single bank transaction or a headline figure measured in billions. It will depend on whether three independent financial records can be reconciled. AMLC reports show how money moved. BIR filings show what income was declared to the government. SALNs show the wealth a public official swore she owned. Each tells only part of the story. Together, they either describe a consistent financial history or expose material inconsistencies requiring constitutional accountability. Sara Duterte deserves the presumption of innocence until allegations against her are proven with solid evidence. An individual like her who holds the nation’s second-highest position, however, is equally obligated to account for her finances under legitimate scrutiny. In the end, the P6.77-billion figure may either prove far less dramatic than political opponents suggest or may reveal

多角的分析

このニュースの経済的側面は、公職者の財政透明性と説明責任という、より広範な問題に根差している。約67億7000万ペソという巨額の取引記録は、フィリピン経済における金融取引の規模と複雑さを示唆している。特に、マネーロンダリング対策法(AMLA)の枠組みにおける「通常取引」と「疑わしい取引」の区別は、金融規制の執行における課題を浮き彫りにする。これらの取引が、合法的な経済活動から生じたものか、それとも潜在的な不正行為の兆候であるかを判断するには、AMLCの報告だけでなく、内国歳入庁(BIR)の納税記録や、公職者の資産申告書(SALN)といった複数の情報源を照合する必要がある。これは、フィリピンの金融システムが、その規模と複雑さゆえに、不正な資金の流れを捕捉し、防止するための継続的な監視と強化が必要であることを示唆している。

投資家にとって、このニュースはフィリピンのガバナンスと透明性に対する懸念を提起する。公職者の財政状況に関する調査は、国の政治的安定性と規制環境の予測可能性に影響を与える可能性がある。副大統領という高位の公職者に関連する巨額の金融取引が、その合法性と申告資産との整合性について疑問視される状況は、外国投資家がフィリピンへの投資を検討する際に、リスク評価の重要な要素となる。特に、マネーロンダリング対策や税務コンプライアンスといった分野での透明性の欠如は、ビジネスリスクを高め、資本の流入に影響を与える可能性がある。投資家は、法制度の執行力と、公職者に対する説明責任のメカニズムが機能しているかどうかを注視する必要がある。

この件は、フィリピン社会における公職者の説明責任と、市民の信頼という根本的な問題に触れている。副大統領という国家の要職にある人物の巨額の金融取引が、その申告資産と一致しない可能性が示唆されることは、多くの国民にとって深刻な懸念事項である。特に、SALNに現金や預金がないと申告されているにもかかわらず、関連する取引が巨額に上るという事実は、一般市民の間に「なぜ公職者は一般市民とは異なる経済活動を行うのか」という疑問を生じさせる。この問題は、公職者が国民の税金によって支えられているという事実と結びつき、政治への不信感や社会的な格差への不満を増幅させる可能性がある。市民は、公職者が自身の財政状況について、透明かつ誠実な説明を行うことを期待しており、その期待が満たされない場合、社会的な緊張が高まることも考えられる。

国民としては、67億7000万ペソという金額が、私たちの税金がどのように使われているのか、あるいは公職者がどのように資産を形成しているのかという疑問を抱かせます。副大統領のSALNに現金や預金がないと書かれているのに、これだけの取引があるというのは、私たち一般市民には理解しがたいことです。これは、公職者が国民に対して、自分たちの財産について正直に開示する義務があるということを改めて考えさせられます。もし、この取引が合法的なものであれば、なぜそれがSALNに反映されないのか、あるいはなぜ納税記録が公開されないのか、という疑問が残ります。国民は、自分たちの代表者が、国民の信頼に応え、透明性を持って行動することを求めています。

背景・歴史的文脈

フィリピンでは、公職者の資産開示義務は、汚職防止と国民の信頼確保のために、憲法および法律で定められている。特に、資産、負債、純資産申告書(SALN)の提出は、公務員倫理法に基づき義務付けられている。マネーロンダリング対策法(AMLA)は、金融機関に一定額以上の取引や疑わしい取引の報告を義務付け、マネーロンダリングやテロ資金供与の防止を目指している。過去にも、高位公職者の資産に関する疑惑は度々浮上しており、その都度、SALNの信頼性や、金融取引の透明性が問われてきた。今回の副大統領に関連する巨額の取引記録は、こうした長年の課題が再び表面化した形であり、司法および立法府による説明責任追及の重要性を示唆している。

原文ソース

Rappler Business