Vietnam Announces Tax and Land Rent Payment Deferral for 2026

Vietnam's Ministry of Finance has announced the implementation of a decree extending the deadline for VAT, corporate income tax, personal income tax, and land rent payments for 2026, aiming to support businesses and individuals and stimulate economic activity.

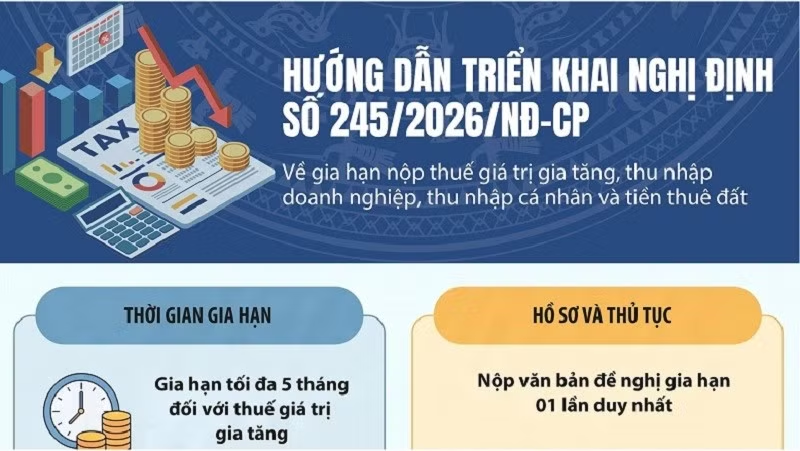

The General Department of Taxation has issued Directive No. 14/CĐ-CT, urging tax authorities at all levels to urgently and synchronously implement Decree No. 245/2026/NĐ-CP. This decree ensures the timely and effective implementation of policies extending the payment deadlines for value-added tax (VAT), corporate income tax, personal income tax, and land rent for 2026. The measure is intended to support businesses and individuals, thereby bolstering economic recovery and growth. This deferral policy is expected to provide significant relief, particularly for small and medium-sized enterprises (SMEs) still recovering from the impacts of the COVID-19 pandemic, and for businesses aiming to resume their operations. By postponing tax and land rent payments for a specific period, companies will have greater flexibility in managing their working capital. Vietnam, operating under a one-party socialist republic system with a market-oriented economy, has frequently introduced fiscal support measures such as tax incentives and payment deferrals to sustain its economic growth. In the face of recent economic fluctuations and global uncertainties, stabilizing the domestic economy and maintaining an attractive investment environment are paramount for the Vietnamese government. Details regarding the specific taxes and land rents covered by this extension, the duration of the deferral, and the application procedures are expected to be announced by the respective tax authorities soon. The General Department of Taxation is also actively promoting understanding of new regulations related to the amended Law on Tax Administration through initiatives like online livestreams. This approach aims to balance efficient tax revenue collection with improved taxpayer services. Source: Nhan Dan

多角的分析

今回の税金・土地賃料納付期限延長は、ベトナム政府が経済成長の維持と国内企業の競争力強化を目指す一環として実施される。特に、グローバルなサプライチェーンの再編やインフレ圧力といった外部要因に直面する中で、国内経済の安定化は喫緊の課題である。企業、特に中小企業にとっては、一時的な資金繰りの緩和は、設備投資や雇用維持に繋がる可能性があり、短期的には消費や投資の活性化に寄与しうる。しかし、延長された税収は将来的に政府の財政に影響を与えるため、その後の財政運営におけるバランスが重要となる。

投資家にとって、この措置はベトナム市場における短期的なリスク軽減要因となりうる。企業収益の改善やキャッシュフローの安定化は、特に景気変動の影響を受けやすいセクターの投資魅力を一時的に高める可能性がある。しかし、これはあくまで一時的な支援策であり、長期的な投資判断においては、ベトナム経済の構造的課題や、政府の財政健全性、そして国際的な経済動向を注視する必要がある。特に、輸出主導型経済であるベトナムにとって、主要貿易相手国の景気動向や地政学リスクへの対応が、投資環境に与える影響は大きい。

この税金・土地賃料納付期限の延長は、特に経営基盤の脆弱な中小企業や個人事業主にとって、事業継続の大きな助けとなる。例えば、ハノイやホーチミン市のような大都市で、家賃や人件費の負担が大きい事業者は、この猶予期間中に資金を確保し、事業の立て直しを図ることができる。また、土地賃料の減免は、製造業や不動産開発といった業種にも恩恵をもたらし、地域経済の活性化に寄与する可能性がある。一方で、この措置が一部の富裕層や大企業に偏らず、広く中小企業や個人に恩恵が行き渡るかどうかが、社会的な公平性の観点から問われる。

今回の政策は、直接的な現金給付ではないものの、多くのベトナム市民、特に自営業者や中小企業経営者にとっては、生活の安定に繋がる重要な支援策となる。例えば、地方都市で小規模な製造業を営む人々は、税金や土地代の支払いが猶予されることで、当面の生活費や従業員の給与を確保しやすくなる。これにより、地域社会における雇用不安の軽減や、地元経済の停滞を防ぐ効果が期待できる。しかし、この恩恵が都市部と地方部、あるいは業種によって格差なく享受されるかどうかが、市民生活の実感として重要となる。

背景・歴史的文脈

ベトナム政府は、社会主義的市場経済への移行以来、経済成長を最優先課題として、外国投資の誘致と国内産業の育成に努めてきた。特に、近年の世界的な経済減速や米中貿易摩擦、そして新型コロナウイルスのパンデミックは、輸出依存度の高いベトナム経済に大きな影響を与えた。これに対し、政府は度々、税制優遇措置や納付期限の延長といった財政・金融支援策を打ち出し、企業活動の維持と経済の安定化を図ってきた。今回の2026年の税金・土地賃料納付期限延長も、こうした一連の経済対策の一環と位置づけられる。これは、ベトナムが国内経済の強靭化と、世界経済の変動に対するレジリエンスを高めようとする姿勢の表れである。

原文ソース

Nhan Dan